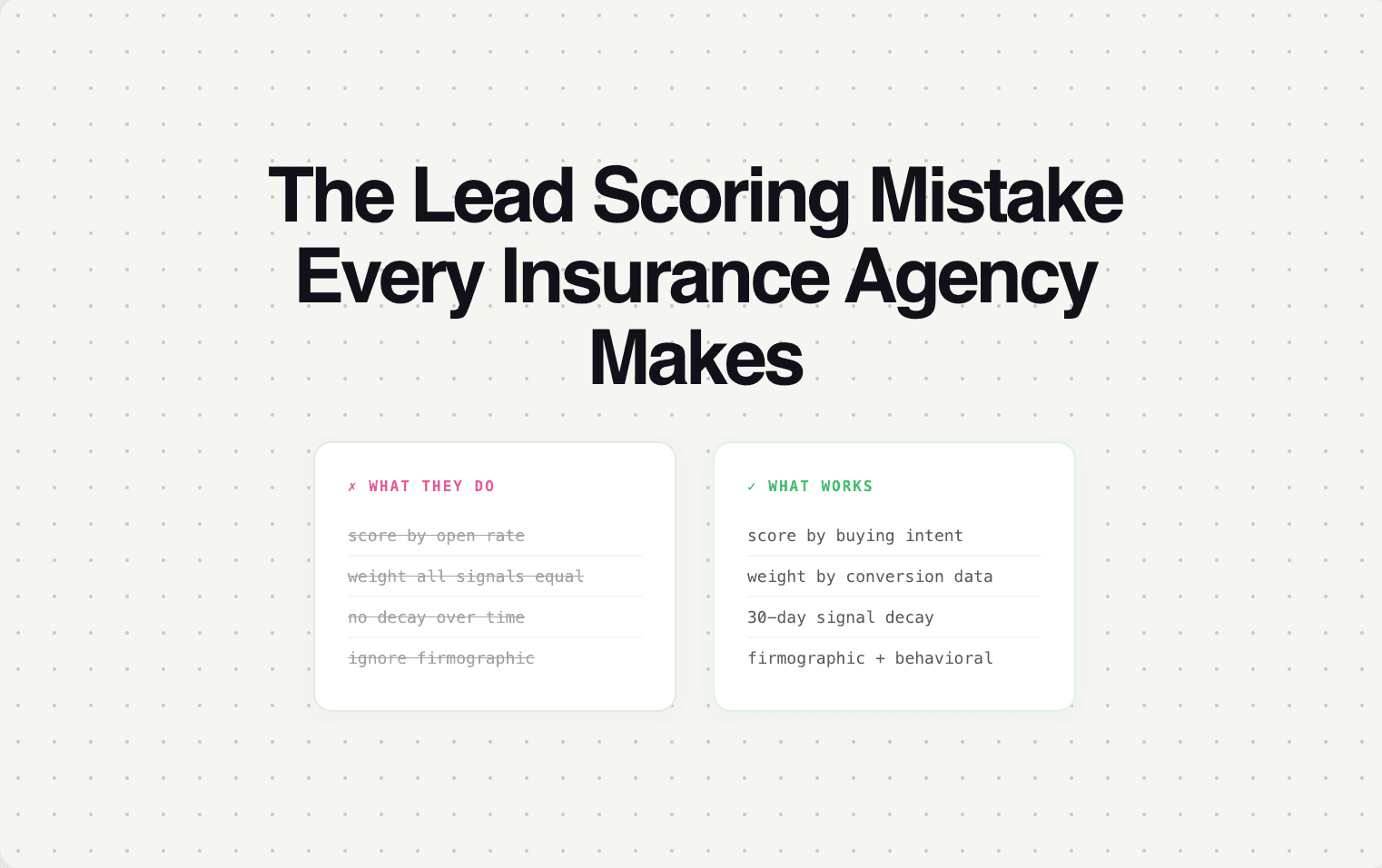

Insurance agencies score leads wrong — and it costs them the policies that actually bind.

The standard approach: a lead comes in, someone glances at it, and makes a gut call. "Big company? Probably a good lead. Single auto policy? Low priority." Or worse, every lead gets equal treatment — the commercial fleet inquiry sits in the same queue as the renter's insurance quote.

The agencies with the highest bind rates don't score on perceived value. They score on likelihood to bind — which is a completely different variable.

Why perceived value ≠ bind probability

A commercial liability inquiry from a 200-employee company looks like a big lead. The potential premium is $50K+. Every agent wants it. But commercial policies have long sales cycles, multiple decision-makers, broker competition, and complex underwriting. The bind rate on cold commercial inquiries is typically 5–10%.

A personal auto quote for a homeowner who just moved to town looks small. $1,500/year premium. Nobody's excited about it. But the bind rate on auto quotes from new-to-area homeowners is 30–40% — because they need coverage immediately and they're actively shopping.

If your agents spend 45 minutes on the commercial lead and 5 minutes on the auto lead, they've optimized for perceived value but not for actual revenue generation. The auto lead was 4–6x more likely to bind.

The signals that predict binding

| Signal | Bind prediction | Why |

|---|---|---|

| Current coverage status: "switching providers" | High (25–35% bind rate) | They already have coverage. They're actively shopping for a better deal. Decision is imminent. |

| Life event trigger: "just bought a home" | High (30–40% bind rate) | They need coverage immediately. Timeline is days, not months. |

| Current coverage status: "no current coverage" | Medium-high (20–30%) | They need coverage. But the urgency depends on why — new driver vs. lapse vs. never had it. |

| Multiple lines requested | High (25–35%) | Someone quoting auto + home + umbrella is serious. They want a relationship, not a single policy. |

| Quote during business hours on a weekday | Higher than evening/weekend | Correlates with active shopping behavior vs. casual browsing. (This varies — test it.) |

| Completed full risk profile on form | High (35–45%) | The more questions they answered, the more committed they are. Form completion depth is the strongest behavioral signal. |

| Abandoned after basic info only | Low (5–10% even with recovery) | Low commitment. May have been doing broad price comparison. |

Building the scoring model

Layer 1: Form completion depth

The simplest and most reliable signal. Someone who completes all risk questions on a multi-step form is fundamentally more committed than someone who enters their email and zip code.

Assign scores based on how far the prospect got:

- Entered email only: 10 points

- Completed basic info (name, email, zip, coverage type): 25 points

- Completed risk questions (vehicle info, property details, health status): 50 points

- Completed full form including contact preferences: 75 points

- Requested a specific agent or scheduled a call: 90 points

Layer 2: Coverage signals

Multi-line requests score higher than single-line. "Switching providers" scores higher than "first-time buyer." Active life events (new home, new car, new baby) score higher than general browsing.

Layer 3: Enrichment-based fit

For commercial lines: company size, industry, and revenue determine whether the prospect is a realistic underwriting fit. A 3-person startup requesting $5M in commercial liability may not be insurable through your carriers.

For personal lines: zip code determines rate competitiveness (your carriers may not be competitive in certain areas), and claims history indicates risk level.

How the score should drive action

| Score range | Lead category | Agent action | Response SLA |

|---|---|---|---|

| 80–100 | Hot — high bind probability | Senior agent immediate follow-up. Full quote preparation. | Under 15 minutes |

| 50–79 | Warm — genuine interest, needs nurture | Agent follow-up same day. Send rate comparison and next steps. | Under 2 hours |

| 25–49 | Cool — early stage or low commitment | Automated nurture. Educational content about coverage options. | Automated response within 1 hour |

| 0–24 | Cold — minimal engagement or poor fit | No agent time. Automated response only. Re-evaluate if they re-engage. | Automated |

This tiering ensures agent time goes to the leads most likely to bind — not the leads that look the most impressive on paper.

The calibration step most agencies skip

After 60 days, pull the data: for each score range, what percentage of leads actually bound a policy? If your 80–100 range is binding at 35% and your 50–79 range is binding at 30%, the model isn't differentiating well enough — refine the scoring weights.

If one specific signal (like "switching providers") is dramatically more predictive than the model's overall score suggests, increase its weight. The model should reflect your actual data, not industry assumptions.

Run this calibration quarterly. Your carrier mix changes, your market changes, and your lead sources change — the model needs to adapt.

Where Surface fits

Surface builds lead scoring into the quote intake flow — form completion depth, coverage signals, enrichment data, and life event triggers all factor into a score that drives routing and response priority. The scoring model calibrates against actual bind data, so it gets more accurate over time.

If your agency treats every lead equally and wonders why your bind rate is stuck at 12%, the scoring model is the fix. Surface was built to make it automatic.